|

CHAPTER XX TRANSITIONAL PROVISIONS

139.Migration of existing taxpayers.

(1) On and from the appointed day, every person registered under any of the existing laws and having a valid Permanent Account Number shall be issued a certificate of registration on provisional basis, subject to such conditions and in such form and manner as may be prescribed, which unless replaced by a final certificate of registration under sub-section (2), shall be liable to be cancelled if the conditions so prescribed are not complied with.

(2) The final certificate of registration shall be granted in such form and manner and subject to such conditions as may be prescribed.

(3) The certificate of registration issued to a person under sub-section (1) shall be deemed to have not been issued if the said registration is cancelled in pursuance of an application filed by such person that he was not liable to registration under section 22 or

section 24.

140.Transitional arrangements for input tax credit.

(1) A registered person, other than a person opting to pay tax under section 10, shall be entitled to take, in his electronic credit ledger, the amount of CENVAT credit carried forward in the return relating to the period ending with the day immediately preceding the appointed day, furnished by him under the existing law in such manner as may be prescribed:

Provided that the registered person shall not be allowed to take credit in the following circumstances, namely:—

(i) where the said amount of credit is not admissible as input tax credit under this Act; or

(ii) where he has not furnished all the returns required under the existing law for the period of six months immediately preceding the appointed date; or

(iii) where the said amount of credit relates to goods manufactured and cleared under such exemption notifications as are notified by the Government.

(2) A registered person, other than a person opting to pay tax under section 10, shall be entitled to take, in his electronic credit ledger, credit of the unavailed CENVAT credit in

respect of capital goods, not carried forward in a return, furnished under the existing law by

him, for the period ending with the day immediately preceding the appointed day in such

manner as may be prescribed:

Provided that the registered person shall not be allowed to take credit unless the said credit was admissible as CENVAT credit under the existing law and is also admissible as input tax credit under this Act.

Explanation.––For the purposes of this sub-section, the expression “unavailed CENVAT credit” means the amount that remains after subtracting the amount of CENVAT credit already availed in respect of capital goods by the taxable person under the existing law

from the aggregate amount of CENVAT credit to which the said person was entitled in respect of the said capital goods under the existing law.

(3) A registered person, who was not liable to be registered under the existing law, or who was engaged in the manufacture of exempted goods or provision of exempted services, or who was providing works contract service and was availing of the benefit of notification

No. 26/2012—Service Tax, dated the 20th June, 2012 or a first stage dealer or a second stage dealer or a registered importer or a depot of a manufacturer, shall be entitled to take, in hiselectronic credit ledger, credit of eligible duties in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock on the appointed day subject to the following conditions, namely:––

(i) such inputs or goods are used or intended to be used for making taxable supplies under this Act;

(ii) the said registered person is eligible for input tax credit on such inputs under this Act;

(iii) the said registered person is in possession of invoice or other prescribed documents evidencing payment of duty under the existing law in respect of such inputs;

(iv) such invoices or other prescribed documents were issued not earlier than twelve months immediately preceding the appointed day; and

(v) the supplier of services is not eligible for any abatement under this Act:

Provided that where a registered person, other than a manufacturer or a supplier of services, is not in possession of an invoice or any other documents evidencing payment of duty in respect of inputs, then, such registered person shall, subject to such conditions,

limitations and safeguards as may be prescribed, including that the said taxable person shall pass on the benefit of such credit by way of reduced prices to the recipient, be allowed to take credit at such rate and in such manner as may be prescribed.

(4) A registered person, who was engaged in the manufacture of taxable as well as exempted goods under the Central Excise Act, 1944 or provision of taxable as well as exempted services under Chapter V of the Finance Act, 1994, but which are liable to tax under this Act,

shall be entitled to take, in his electronic credit ledger,—

(a) the amount of CENVAT credit carried forward in a return furnished under the existing law by him in accordance with the provisions of sub-section (1); and

(b) the amount of CENVAT credit of eligible duties in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock on the appointed day, relating to such exempted goods or services, in accordance with the

provisions of sub-section (3).

(5) A registered person shall be entitled to take, in his electronic credit ledger, credit of eligible duties and taxes in respect of inputs or input services received on or after the appointed day but the duty or tax in respect of which has been paid by the supplier under the

existing law, subject to the condition that the invoice or any other duty or tax paying document of the same was recorded in the books of account of such person within a period of thirty days from the appointed day:

Provided that the period of thirty days may, on sufficient cause being shown, be extended by the Commissioner for a further period not exceeding thirty days:

Provided further that said registered person shall furnish a statement, in such manner as may be prescribed, in respect of credit that has been taken under this sub-section.

(6) A registered person, who was either paying tax at a fixed rate or paying a fixed amount in lieu of the tax payable under the existing law shall be entitled to take, in his electronic credit ledger, credit of eligible duties in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock on the appointed day subject to the following conditions, namely:––

(i) such inputs or goods are used or intended to be used for making taxable supplies under this Act;

(ii) the said registered person is not paying tax under section 10;

(iii) the said registered person is eligible for input tax credit on such inputs under this Act;

(iv) the said registered person is in possession of invoice or other prescribed documents evidencing payment of duty under the existing law in respect of inputs; and

(v) such invoices or other prescribed documents were issued not earlier than twelve months immediately preceding the appointed day.

(7) Notwithstanding anything to the contrary contained in this Act, the input tax credit on account of any services received prior to the appointed day by an Input Service Distributor shall be eligible for distribution as credit under this Act even if the invoices relating to such

services are received on or after the appointed day.

(8) Where a registered person having centralised registration under the existing law has obtained a registration under this Act, such person shall be allowed to take, in his electronic credit ledger, credit of the amount of CENVAT credit carried forward in a return,

furnished under the existing law by him, in respect of the period ending with the day immediately preceding the appointed day in such manner as may be prescribed:

Provided that if the registered person furnishes his return for the period ending with the day immediately preceding the appointed day within three months of the appointed day, such credit shall be allowed subject to the condition that the said return is either an original

return or a revised return where the credit has been reduced from that claimed earlier:

Provided further that the registered person shall not be allowed to take credit unless he said amount is admissible as input tax credit under this Act:

Provided also that such credit may be transferred to any of the registered persons having the same Permanent Account Number for which the centralised registration was obtained under the existing law.

(9) Where any CENVAT credit availed for the input services provided under the existing aw has been reversed due to non-payment of the consideration within a period of three months, such credit can be reclaimed subject to the condition that the registered person has made the payment of the consideration for that supply of services within a period of three months from the appointed day.

(10) The amount of credit under sub-sections (3), (4) and (6) shall be calculated in such manner as may be prescribed.

Explanation 1.—For the purposes of sub-sections (3), (4) and (6), the expression “eligible duties” means––

(i) the additional duty of excise leviable under section 3 of the Additional Duties of Excise (Goods of Special Importance) Act, 1957;

(ii) the additional duty leviable under sub-section (1) of section 3 of the Customs Tariff Act, 1975;

(iii) the additional duty leviable under sub-section (5) of section 3 of the Customs Tariff Act, 1975;

(iv) the additional duty of excise leviable under section 3 of the Additional Duties of Excise (Textile and Textile Articles) Act, 1978;

(v) the duty of excise specified in the First Schedule to the Central Excise Tariff Act, 1985;

(vi) the duty of excise specified in the Second Schedule to the Central Excise Tariff Act, 1985; and

(vii) the National Calamity Contingent Duty leviable under section 136 of the Finance Act, 2001, in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock on the appointed day.

Explanation 2.—For the purposes of sub-section (5), the expression “eligible duties and taxes” means––

(i) the additional duty of excise leviable under section 3 of the Additional Duties of Excise (Goods of Special Importance) Act, 1957;

(ii) the additional duty leviable under sub-section (1) of section 3 of the Customs Tariff Act, 1975;

(iii) the additional duty leviable under sub-section (5) of section 3 of the Customs ariff Act, 1975;

(iv) the additional duty of excise leviable under section 3 of the Additional Duties of Excise (Textile and Textile Articles) Act, 1978;

(v) the duty of excise specified in the First Schedule to the Central Excise Tariff Act, 1985;

(vi) the duty of excise specified in the Second Schedule to the Central Excise Tariff Act, 1985;

(vii) the National Calamity Contingent Duty leviable under section 136 of them Finance Act, 2001; and

(viii) the service tax leviable under section 66B of the Finance Act, 1994, in respect of inputs and input services received on or after the appointed day.

141.Transitional provisions relating to job work.

(1) Where any inputs received at a place of business had been removed as such or removed after being partially processed to a job worker for further processing, testing, repair, reconditioning or any other purpose in accordance with the provisions of existing law prior to the appointed day and such inputs are returned to the said place on or after the appointed day, no tax shall be payable if such inputs, after completion of the job work or otherwise, are returned to the said place within six months from the appointed day:

Provided that the period of six months may, on sufficient cause being shown, be extended by the Commissioner for a further period not exceeding two months:

Provided further that if such inputs are not returned within the period specified in this sub-section, the input tax credit shall be liable to be recovered in accordance with the provisions of clause (a) of sub-section (8) of section 142.

(2) Where any semi-finished goods had been removed from the place of business to any other premises for carrying out certain manufacturing processes in accordance with the provisions of existing law prior to the appointed day and such goods (hereafter in this

section referred to as “the said goods”) are returned to the said place on or after the appointed day, no tax shall be payable, if the said goods, after undergoing manufacturing processes or otherwise, are returned to the said place within six months from the appointed

day:

Provided that the period of six months may, on sufficient cause being shown, be extended by the Commissioner for a further period not exceeding two months:

Provided further that if the said goods are not returned within the period specified in this sub-section, the input tax credit shall be liable to be recovered in accordance with the provisions of clause (a) of sub-section (8) of section 142:

Provided also that the manufacturer may, in accordance with the provisions of the existing law, transfer the said goods to the premises of any registered person for the purpose of supplying therefrom on payment of tax in India or without payment of tax for exports within the period specified in this sub-section.

(3) Where any excisable goods manufactured at a place of business had been removed without payment of duty for carrying out tests or any other process not amounting to manufacture, to any other premises, whether registered or not, in accordance with the provisions of existing law prior to the appointed day and such goods, are returned to the said place on or after the appointed day, no tax shall be payable if the said goods, after undergoing tests or any other process, are returned to the said place within six months from the appointed

day:

Provided that the period of six months may, on sufficient cause being shown, be extended by the Commissioner for a further period not exceeding two months:

Provided further that if the said goods are not returned within the period specified in this sub-section, the input tax credit shall be liable to be recovered in accordance with the provisions of clause (a) of sub-section (8) of section 142:

Provided also that the manufacturer may, in accordance with the provisions of the existing law, transfer the said goods from the said other premises on payment of tax in India or without payment of tax for exports within the period specified in this sub-section.

(4) The tax under sub-sections (1), (2) and (3) shall not be payable, only if the manufacturer and the job worker declare the details of the inputs or goods held in stock by the job worker on behalf of the manufacturer on the appointed day in such form and manner

and within such time as may be prescribed.

142.Miscellaneous transitional provisions.

(1) Where any goods on which duty, if any, had been paid under the existing law at the time of removal thereof, not being earlier than six months prior to the appointed day, are returned to any place of business on or after the appointed day, the registered person shall be ligible for refund of the duty paid under the existing law where such goods are returned by a person, other than a registered person, to the said place of business within a period of six months from the appointed day and such goods are identifiable to the satisfaction of the

proper officer:

Provided that if the said goods are returned by a registered person, the return of such goods shall be deemed to be a supply.

(2) (a) where, in pursuance of a contract entered into prior to the appointed day, the price of any goods or services or both is revised upwards on or after the appointed day, the registered person who had removed or provided such goods or services or both shall issue to the recipient a supplementary invoice or debit note, containing such particulars as may be prescribed, within thirty days of such price revision and for the purposes of this Act such supplementary invoice or debit note shall be deemed to have been issued in respect of an

outward supply made under this Act;

(b) where, in pursuance of a contract entered into prior to the appointed day, the price of any goods or services or both is revised downwards on or after the appointed day, the registered person who had removed or provided such goods or services or both may issue to the recipient a credit note, containing such particulars as may be prescribed, within thirtyn days of such price revision and for the purposes of this Act such credit note shall be deemed to have been issued in respect of an outward supply made under this Act:

Provided that the registered person shall be allowed to reduce his tax liability onaccount of issue of the credit note only if the recipient of the credit note has reduced his input tax credit corresponding to such reduction of tax liability.

(3) Every claim for refund filed by any person before, on or after the appointed day, for refund of any amount of CENVAT credit, duty, tax, interest or any other amount paid under the existing law, shall be disposed of in accordance with the provisions of existing law and any amount eventually accruing to him shall be paid in cash, notwithstanding anything to the contrary contained under the provisions of existing law other than the provisions of sub-section (2) of section 11B of the Central Excise Act, 1944:

Provided that where any claim for refund of CENVAT credit is fully or partially rejected, the amount so rejected shall lapse:

Provided further that no refund shall be allowed of any amount of CENVAT credit where the balance of the said amount as on the appointed day has been carried forwardn under this Act.

(4) Every claim for refund filed after the appointed day for refund of any duty or tax paid under existing law in respect of the goods or services exported before or after the appointed day, shall be disposed of in accordance with the provisions of the existing law:

Provided that where any claim for refund of CENVAT credit is fully or partially rejected, the amount so rejected shall lapse:

Provided further that no refund shall be allowed of any amount of CENVAT credit where the balance of the said amount as on the appointed day has been carried forward under this Act.

(5) Every claim filed by a person after the appointed day for refund of tax paid under the existing law in respect of services not provided shall be disposed of in accordance with the provisions of existing law and any amount eventually accruing to him shall be paid in cash, notwithstanding anything to the contrary contained under the provisions of existing law other than the provisions of sub-section (2) of section 11B of the Central Excise Act, 1944.

(6) (a) every proceeding of appeal, review or reference relating to a claim for CENVAT credit initiated whether before, on or after the appointed day under the existing law shall be disposed of in accordance with the provisions of existing law, and any amount of credit found to be admissible to the claimant shall be refunded to him in cash, notwithstanding anything to the contrary contained under the provisions of existing law other than the provisions of sub-section (2) of section 11B of the Central Excise Act, 1944 and the amount

rejected, if any, shall not be admissible as input tax credit under this Act:

Provided that no refund shall be allowed of any amount of CENVAT credit where the balance of the said amount as on the appointed day has been carried forward under this Act;

(b) every proceeding of appeal, review or reference relating to recovery of CENVAT credit initiated whether before, on or after the appointed day under the existing law shall be disposed of in accordance with the provisions of existing law and if any amount of credit

becomes recoverable as a result of such appeal, review or reference, the same shall, unless recovered under the existing law, be recovered as an arrear of tax under this Act and them amount so recovered shall not be admissible as input tax credit under this Act.

(7) (a) every proceeding of appeal, review or reference relating to any output duty or

tax liability initiated whether before, on or after the appointed day under the existing law, shall be disposed of in accordance with the provisions of the existing law, and if any amount becomes recoverable as a result of such appeal, review or reference, the same shall,

unless recovered under the existing law, be recovered as an arrear of duty or tax under this Act and the amount so recovered shall not be admissible as input tax credit under this Act.

(b) every proceeding of appeal, review or reference relating to any output duty or tax liability initiated whether before, on or after the appointed day under the existing law, shall be disposed of in accordance with the provisions of the existing law, and any amount found to be admissible to the claimant shall be refunded to him in cash, notwithstanding anything to he contrary contained under the provisions of existing law other than the provisions of sub-section (2) of section 11B of the Central Excise Act, 1944 and the amount rejected, if any,

shall not be admissible as input tax credit under this Act.

(8) (a) where in pursuance of an assessment or adjudication proceedings instituted, whether before, on or after the appointed day, under the existing law, any amount of tax, interest, fine or penalty becomes recoverable from the person, the same shall, unless recovered

under the existing law, be recovered as an arrear of tax under this Act and the amount so recovered shall not be admissible as input tax credit under this Act;

(b) where in pursuance of an assessment or adjudication proceedings instituted, whether before, on or after the appointed day, under the existing law, any amount of tax, interest, fine or penalty becomes refundable to the taxable person, the same shall be refunded to him in

cash under the said law, notwithstanding anything to the contrary contained in the said law other than the provisions of sub-section (2) of section 11B of the Central Excise Act, 1944 and the amount rejected, if any, shall not be admissible as input tax credit under this Act.

(9) (a) where any return, furnished under the existing law, is revised after the appointed day and if, pursuant to such revision, any amount is found to be recoverable or any amount of CENVAT credit is found to be inadmissible, the same shall, unless recovered under the

existing law, be recovered as an arrear of tax under this Act and the amount so recovered shall not be admissible as input tax credit under this Act;

(b) where any return, furnished under the existing law, is revised after the appointed day but within the time limit specified for such revision under the existing law and if, pursuant to such revision, any amount is found to be refundable or CENVAT credit is found to be

admissible to any taxable person, the same shall be refunded to him in cash under the existing aw, notwithstanding anything to the contrary contained in the said law other than the provisions of sub-section (2) of section 11B of the Central Excise Act, 1944 and the amount rejected, if any, shall not be admissible as input tax credit under this Act.

(10) Save as otherwise provided in this Chapter, the goods or services or both supplied on or after the appointed day in pursuance of a contract entered into prior to the appointed day shall be liable to tax under the provisions of this Act.

(11) (a) notwithstanding anything contained in section 12, no tax shall be payable on goods under this Act to the extent the tax was leviable on the said goods under the Value Added Tax Act of the State;

(b) notwithstanding anything contained in section 13, no tax shall be payable onservices under this Act to the extent the tax was leviable on the said services under Chapter V of the Finance Act, 1994;

(c) where tax was paid on any supply both under the Value Added Tax Act and under Chapter V of the Finance Act, 1994, tax shall be leviable under this Act and the taxable person shall be entitled to take credit of value added tax or service tax paid under the existing law to

the extent of supplies made after the appointed day and such credit shall be calculated in such manner as may be prescribed.

(12) Where any goods sent on approval basis, not earlier than six months before the appointed day, are rejected or not approved by the buyer and returned to the seller on or after the appointed day, no tax shall be payable thereon if such goods are returned within six

months from the appointed day:

Provided that the said period of six months may, on sufficient cause being shown, be extended by the Commissioner for a further period not exceeding two months:

Provided further that the tax shall be payable by the person returning the goods if such goods are liable to tax under this Act, and are returned after a period specified in this sub-section:

Provided also that tax shall be payable by the person who has sent the goods on approval basis if such goods are liable to tax under this Act, and are not returned within a period specified in this sub-section.

(13) Where a supplier has made any sale of goods in respect of which tax was required to be deducted at source under any law of a State or Union territory relating to Value Added Tax and has also issued an invoice for the same before the appointed day, no deduction of tax

at source under section 51 shall be made by the deductor under the said section where payment to the said supplier is made on or after the appointed day.

Explanation.––For the purposes of this Chapter, the expressions “capital goods”, “Central Value Added Tax (CENVAT) credit”, “first stage dealer”, “second stage dealer”, or “manufacture” shall have the same meaning as respectively assigned to them in the Central Excise Act, 1944 or the rules made thereunder.

|

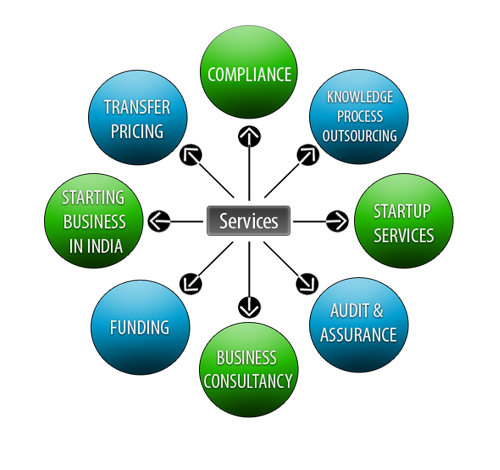

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

Lets Enhance your Profits by Our Services