We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

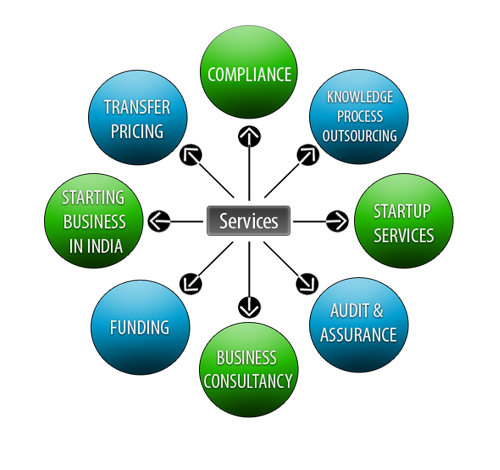

Lets Enhance your Profits by Our Services