|

CHAPTER XIIB VERIFICATION OF IDENTITY AND COMPLIANCE

99B. (1) The proper officer, authorised in this behalf by the Principal Commissioner of Customs or the Commissioner of Customs, as the case may be, may, for the purposes of ascertaining compliance of the provisions of this Act or any other law for the time being in force, require a person, whose verification he considers necessary for protecting the interest of revenue or for preventing smuggling, to do all or any of the following, namely:–– (a) undergo authentication, or furnish proof of possession of Aadhaar number, in such manner and within such time as may be prescribed; (b) submit such other document or information, in such manner and within such time as may be prescribed: Provided that where such person has not been assigned the Aadhaar number, or where so assigned, but authentication of such person has failed due to technical reasons or for reasons beyond his control, then, he shall be provided an opportunity to furnish such other alternative and viable means of identification in such form and manner and within such time as may be prescribed. (2) The provisions of sub-section (1) shall not apply to such person or class of persons as may be prescribed. (3) Notwithstanding anything contained in any other provisions of this Act, where the Principal Commissioner of Customs or the Commissioner of Customs comes to the conclusion, based on reasons to be recorded in writing, that the person referred to in sub-section (1) has–– (i) failed to comply with the requirements of the said sub-section or submitted incorrect documents or information under the said sub-section, he may, by order, suspend–– (a) clearance of imported goods or export goods; (b) sanction of refund; (c) sanction of drawback; (d) exemption from duty; (e) licence or registration granted under this Act; or (f) any benefit, monetary or otherwise, arising out of import or export, relating to such person, subject to such conditions as may be prescribed; (ii) failed authentication as required under the said sub-section, he may, by order, direct that such person shall not have the benefit of any of the items specified in sub-clauses (a) to (f) of clause (i). (4) The order of suspension under sub-section (3) shall remain in force until the person concerned complies with the requirements of sub-section (1) or furnishes correct document or information thereunder. Explanation.—For the purposes of this section, the expression “Aadhaar number” shall have the same meaning as assigned to it in clause (a) of section 2 of the Aadhaar (Targeted Delivery of Financial and Other Subsidies, Benefits and Services) Act, 2016.’. 72. In section 103 of the Customs Act,— (i) for sub-section (1), the following sub-section shall be substituted, namely:– “(1) Where the proper officer has reason to believe that any person referred to in sub-section (2) of section 100 has any goods liable to confiscation secreted inside his body, he may detain such person and shall,–– (a) with the prior approval of the Deputy Commissioner of Customs or Assistant Commissioner of Customs, as soon as practicable, screen or scan such person using such equipment as may be available at the customs station, but without prejudice to any of the rights available to such person under any other law for the time being in force, including his consent for such screening or scanning, and forward a report of such screening or scanning to the nearest magistrate if such goods appear to be secreted inside his body; or (b) produce him without unnecessary delay before the nearest magistrate.”; (ii) in sub-section (6), after the words “Where on receipt of a report”, the words, brackets, letter and figure “from the proper officer under clause (a) of sub-section (1) or” shall be inserted. 73. In section 104 of the Customs Act, –– (i) in sub-section (1), the words “in India or within the Indian customs waters” shall be omitted; (ii) in sub-section (4),–– (A) in clause (b), for the word “rupees,”, the words “rupees; or” shall be substituted; (B) after clause (b), the following clauses shall be inserted, namely:— “(c) fraudulently availing of or attempting to avail drawback or any exemption from duty provided under this Act, where the amount of drawback or exemption from duty exceeds fifty lakh rupees; or (d) fraudulently obtaining an instrument for the purposes of this Act or the Foreign Trade (Development and Regulation) Act, 1992, and such instrument is utilised under this Act, where duty relatable to such utilisation of instrument exceeds fifty lakh rupees,”; (iii) in sub-section (6),–– (A) in clause (d), for the word “rupees,”, the words “rupees; or” shall be substituted; (B) after clause (d), the following clause shall be inserted, namely:— “(e) fraudulently obtaining an instrument for the purposes of this Act or the Foreign Trade (Development and Regulation) Act, 1992, and such instrument is utilised under this Act, where duty relatable to such utilisation of instrument exceeds fifty lakh rupees,”;

‘Explanation.––For the purposes of this section, the expression “instrument” shall have the same meaning as assigned to it in Explanation 1 to section 28AAA.’.

(i) in sub-section (1), for the proviso, the following provisos shall be substituted, namely:— “Provided that where it is not practicable to remove, transport, store or take physical possession of the seized goods for any reason, the proper officer may give custody of the seized goods to the owner of the goods or the beneficial owner or any person holding himself out to be the importer, or any other person from whose custody such goods have been seized, on execution of an undertaking by such person that he shall not remove, part with, or otherwise deal with the goods except with the previous permission of such officer: Provided further that where it is not practicable to seize any such goods, the proper officer may serve an order on the owner of the goods or the beneficial owner or any person holding himself out to be importer, or any other person from whose custody such goods have been found, directing that such person shall not remove, part with, or otherwise deal with such goods except with the previous permission of such officer.”; (ii) after sub-section (4), the following sub-section shall be inserted, namely:— “(5) Where the proper officer, during any proceedings under the Act, is of the opinion that for the purposes of protecting the interest of revenue or preventing smuggling, it is necessary so to do, he may, with the approval of the Principal Commissioner of Customs or Commissioner of Customs, by order in writing, provisionally attach any bank account for a period not exceeding six months: Provided that the Principal Commissioner of Customs or Commissioner of Customs may, for reasons to be recorded in writing, extend such period to a further period not exceeding six months and inform such extension of time to the person whose bank account is provisionally attached, before the expiry of the period so specified.”. 75. In section 110A of the Customs Act,— (i) in the marginal heading, after the words ‘‘things seized’’, the words ‘‘or bank account provisionally attached’’ shall be inserted; (ii) after the words “documents or things seized”, the words “or bank account provisionally attached” shall be inserted; (iii) after the words ‘‘to the owner’’, the words ‘‘or the bank account holder’’ shall be inserted. 76. After section 114AA of the Customs Act, the following section shall be inserted,namely:–– ‘114AB. Where any person has obtained any instrument by fraud, collusion, wilful misstatement or suppression of facts and such instrument has been utilised by such person or any other person for discharging duty, the person to whom the instrument was issued shall be liable for penalty not exceeding the face value of such instrument. Explanation.––For the purposes of this section, the expression “instrument” shall have the same meaning as assigned to it in the Explanation 1 to section 28AAA.’. 77. In section 117 of the Customs Act, for the words “one lakh rupees”, the words “four lakh rupees” shall be substituted. 78. In section 125 of the Customs Act, in sub-section (1), in the first proviso, for the words “the provisions of this section shall not apply”, the words “no such fine shall be imposed” shall be substituted. 79. In section 135 of the Customs Act,–– (i) in sub-section (1),— (a) in clause (d), for the words ‘‘export of goods,’’, the words ‘‘export of goods; or’’ shall be substituted; (b) after clause (d), the following clause shall be inserted, namely:— “(e) obtains an instrument from any authority by fraud, collusion, wilful misstatement or suppression of facts and such instrument has been utilised by such person or any other person,”; (c) in item (i),— (I) in sub-item (D), for the words ‘‘of rupees,’’, the words ‘‘of rupees; or’’ shall be substituted; (II) after sub-item (D), the following sub-item shall be inserted, namely:— “(E) obtaining an instrument from any authority by fraud, collusion, wilful misstatement or suppression of facts and such instrument has been utilised by any person, where the duty relatable to utilisation of the instrument exceeds fifty lakh rupees,”. (ii) after sub-section (3), the following Explanation shall be inserted, namely:— ‘Explanation.–– For the purposes of this section, the expression “instrument” shall have the same meaning as assigned to it in the Explanation 1 to section 28AAA.’. 80. In section 149 of the Customs Act, after the words “custom house to be amended”, the words “in such form and manner, within such time, subject to such restrictions and conditions, as may be prescribed” shall be inserted. 81. In section 157 of the Customs Act, in sub-section (2),–– (i) after clause (k), the following clause shall be inserted, namely:–– “(ka) the manner of authentication and the time limit for such authentication, the document or information to be furnished and the manner of submitting such document or information and the time limit for such submission, the form and the manner of furnishing alternative means of identification and the time limit for furnishing such identification, person or class of persons to be exempted and conditions subject to which suspension may be made, under Chapter XIIB;”; (ii) after clause (m), the following clause shall be inserted, namely:–– “(n) the form and manner, the time limit and the restrictions and conditions for amendment of any document under section 149.”. 82. In section 158 of the Customs Act, in sub-section (2), in clause (ii), for the words “fifty thousand rupees”, the words “two lakh rupees” shall be substituted. 83. (1) The notifications of the Government of India in the Ministry of Finance (Department of Revenue) numbers G.S.R. 423(E), dated the 1st June, 2011, G.S.R. 499 (E), dated the 1st July, 2011 and G.S.R. 185(E), dated the 17th March, 2012 issued by the Central Government under sub-section (1) of section 25 of the Customs Act, 1962, shall stand amended and shall be deemed to have been amended in the manner as specified in the Second Schedule, on and from the date mentioned in column (4) of that Schedule, against each of such notifications, retrospectively, and accordingly, notwithstanding anything contained in any judgment, decree or order of any court, tribunal or other authority, any action taken or anything done or purported to have been taken or done under the said notifications, shall be deemed to be, and always to have been, for all purposes, as validly and effectively taken or done as if the notifications as amended by this sub-section had been in force at all material times. (2) For the purposes of sub-section (1), the Central Government shall have and shall be deemed to have the power to amend the notifications referred to in the said sub-section with retrospective effect as if the Central Government had the power to amend the said notifications under sub-section (1) of section 25 of the Customs Act, retrospectively, at all material times. 84. (1) The notification of the Government of India in the Ministry of Finance (Department of Revenue) number G.S.R. 785(E), dated the 30th June, 2017 issued by the Central Government under sub-section (1) of section 25 of the Customs Act, 1962 and subsection (12) of section 3 of the Customs Tariff Act, 1975, shall stand amended and shall be deemed to have been amended in the manner as specified in the Third Schedule, on and from the date mentioned in column (4) of that Schedule and accordingly, notwithstanding anything contained in any judgment, decree or order of any court, tribunal or other authority, any action taken or anything done or purported to have been taken or done under the said notification, shall be deemed to be, and always to have been, for all purposes, as validly and effectively taken or done as if the notification as amended by this sub-section had been in force at all material times.

|

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

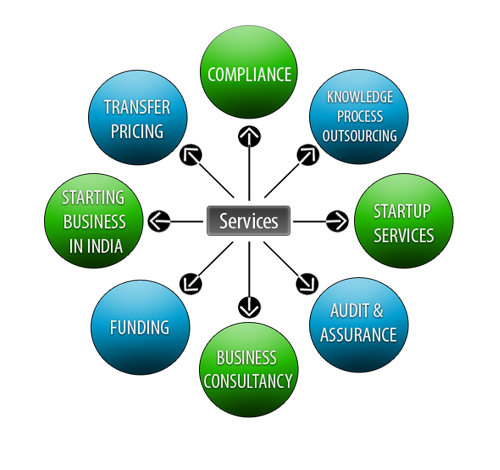

Lets Enhance your Profits by Our Services