|

19. Tax of deceased person payable by legal representative. (1) Where a person dies, his executor, administrator or other legal representative shall be liable to pay out of the estate of the deceased person, to the extent to which the estate is capable of meeting the charge, the wealth-tax assessed as payable by such person, or any sum, which would have been payable by him under this Act if he had not died. (2) Where a person dies without having furnished a return under the provisions of section 14 or after having furnished a return which the 85[Assessing Officer] has reason to believe to be incorrect or incomplete, the 85[Assessing Officer] may make an assessment of the net wealth of such person and determine the wealth-tax payable by the person on the basis of such assessment, and for this purpose may, by the issue of the appropriate notice which would have had to be served upon the deceased person if he had survived, require from the executor, administrator or other legal representative of the deceased person any accounts, documents or other evidence which might under the provisions of section 16 have been required from the deceased person. (3) The provisions of sections 14, 15 and 17 shall apply to an executor, administrator or other legal representative as they apply to any person referred to in those sections. |

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

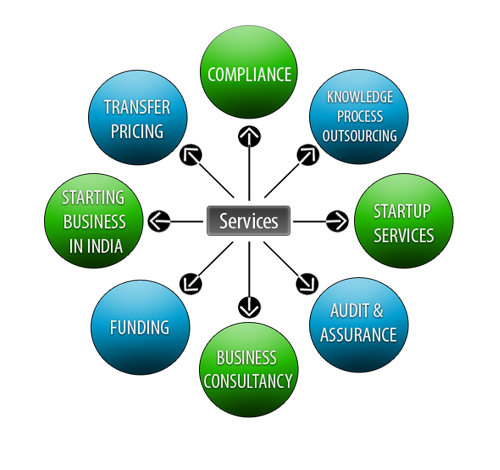

Lets Enhance your Profits by Our Services