|

35. Rectification of mistakes. (1) With a view to rectifying any mistake apparent from the record—

(2) Where the amount of tax, penalty or interest determined as a result of the first appeal or revision against the order referred to in sub-clause (iii) of clause (m) of section 2 80[, as it existed immediately before its amendment by the Finance Act, 1992,] is paid within six months of the date of the order passed in such appeal or revision, the 81[Assessing Officer] may, notwithstanding anything to the contrary in this Act, rectify the assessment by allowing a deduction to the extent the tax, penalty or interest so paid stood disallowed therein as if such rectification were a rectification of a mistake apparent from the record. (3) Subject to the other provisions of this section, the authority concerned—

(4) An amendment, which has the effect of enhancing an assessment or reducing a refund or otherwise increasing the liability of the assessee, shall not be made under this section unless the authority concerned has given notice to the assessee of its intention so to do and has allowed the assessee a reasonable opportunity of being heard. (5) Where an amendment is made under this section, an order shall be passed in writing by the wealth-tax authority concerned or the Tribunal, as the case may be. (6) Where any such amendment has the effect of enhancing the assessment or reducing a refund already made, the 86[Assessing Officer] shall serve on the assessee a notice of demand in the prescribed form specifying the sum payable and such notice of demand shall be deemed to be issued under section 30 and the provisions of this Act shall apply accordingly. 87[(6A) Where any amendment made by the Valuation Officer under clause (aa)* of sub-section (1) has the effect of enhancing the valuation of any asset, he shall send a copy of his order to the86[Assessing Officer] who shall thereafter proceed to amend the order of assessment in conformity with the order of the Valuation Officer and the provisions of sub-section (6) shall apply accordingly.] (7) No amendment under this section shall be made after the expiry of four years—

90[(7A) Notwithstanding anything contained in sub-section (7), where the valuation of any asset has been enhanced by the Valuation Officer under this section, the consequential amendment to the order of assessment may be made by the 91[Assessing Officer] at any time before the expiry of one year from the date of the order of the Valuation Officer under this section.] (8) Where any matter has been considered and decided in a proceeding by way of an appeal or revision relating to an order referred to in sub-section (1), the authority passing such order may, notwithstanding anything contained in any other law for the time being in force, amend the order under this section in relation to any matter other than the matter which has been so considered and decided.] |

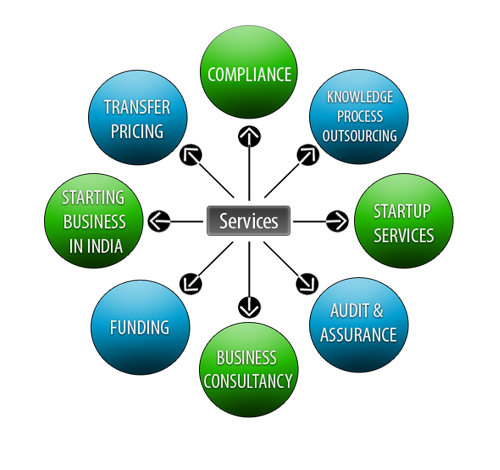

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

Lets Enhance your Profits by Our Services