|

18A. Penalty for failure to answer questions, sign statements, furnish information, allow inspection, etc. (1) If any person,—

he shall pay, by way of penalty, a sum which shall not be less than five hundred rupees but which may extend to ten thousand rupees for each such default or failure : Provided that no penalty shall be imposable under clause (c) if the person proves that there was reasonable cause for the said failure. (2) If a person fails to furnish in due time any statement or information which such person is bound to furnish to the Assessing Officer under section 38, he shall pay, by way of penalty, a sum which shall not be less than one hundred rupees but which may extend to two hundred rupees for every day during which the failure continues : Provided that no penalty shall be imposable under this sub-section if the person proves that there was reasonable cause for the said failure. (3) Any penalty imposable under sub-section (1) or sub-section (2) shall be imposed—

(4) No order under this section shall be passed by any wealth-tax authority referred to in sub-section (3) unless the person on whom the penalty is proposed to be imposed has been heard, or has been given a reasonable opportunity of being heard in the matter, by such authority. Explanation.—In this section, "wealth-tax authority" includes a Director General, Director, 62[Joint] Director, Assistant Director 63[or Deputy Director] and a Valuation Officer while exercising the powers vested in a court under the Code of Civil Procedure, 1908 (5 of 1908), when trying a suit in respect of the matters specified in sub-section (1) of section 37.] |

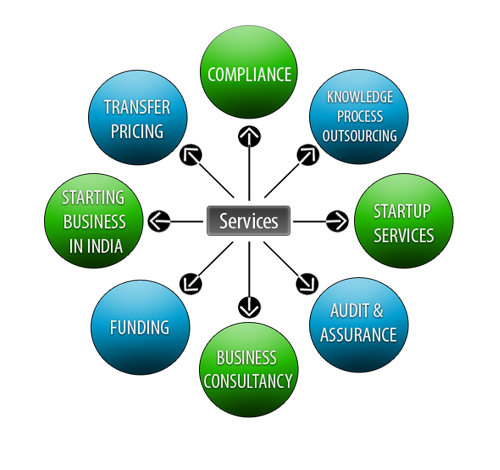

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

Lets Enhance your Profits by Our Services