|

3. Charge of wealth-tax . [(1)] [Subject to the other provisions contained in this Act], there shall be charged for every [assessment year] commencing on and from the first day of April, 1957 [but before the first day of April, 1993], a tax (hereinafter referred to as wealth-tax) in respect of the net wealth on the corresponding valuation date of every individual, Hindu undivided family and company at the rate or rates specified in [Schedule I]. [(2) Subject to the other provisions contained in this Act, there shall be charged for every assessment year commencing on and from the 1st day of April, 1993, [but before the 1st day of April, 2016], wealth-tax in respect of the net wealth on the corresponding valuation date of every individual, Hindu undivided family and company, at the rate of one per cent of the amount by which the net wealth exceeds fifteen lakh rupees:] [Provided that in the case of every assessment year commencing on and from the 1st day of April, 2010, the provisions of this section shall have effect as if for the words "fifteen lakh rupees", the words "thirty lakh rupees" had been substituted.] |

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

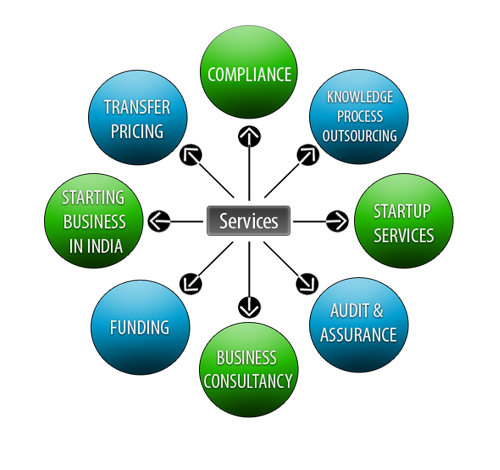

Lets Enhance your Profits by Our Services