|

161. Treatment of retention payments

Notwithstanding anything contained in section 12 and 13, no tax shall be payable on the supply of goods and/or services made before the appointed day where a part consideration for the said supply is received on or after the appointed day, but the full duty or tax payable on such supply has already been paid under the earlier law.

Notwithstanding anything contained in section 12 and 13, no tax shall be payable on the supply of goods and/or services made before the appointed day where a part consideration for the said supply is received on or after the appointed day, but the full duty or tax payable on such supply has already been paid under the earlier law.

|

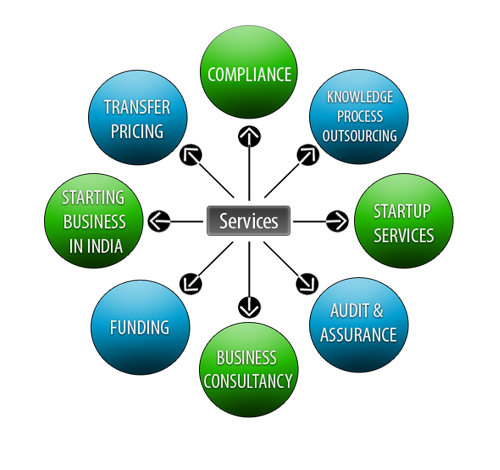

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

Lets Enhance your Profits by Our Services