|

Finalization of proceedings relating to output duty or tax liability (1)Every proceeding of appeal, revision, review or reference relating to any output duty or tax liability initiated whether before, on or after the appointed day, shall be disposed of in accordance with the provisions of the earlier law, and if any amount becomes recoverable as a result of such appeal, revision, review or reference, the same shall be recovered as an arrear of duty or tax under this Act and amount so recovered shall not be admissible as input tax credit under this Act. (2)Every proceeding of appeal, revision, review or reference relating to any output duty or tax liability initiated whether before, on or after the appointed day, shall be disposed of in accordance with the provisions of the earlier law, and any amount found to be admissible to the claimant shall be refunded to him in cash, notwithstanding anything to the contrary contained under the provisions of earlier law other than the provisions of sub-section (2) of section 11B of the Central Excise Act, 1944and shall not be admissible as input tax credit under this Act. (CGST Law) (1)Every proceeding of appeal, revision, review or reference relating to any output tax liability initiated whether before, on or after the appointed day, shall be disposed of in accordance with the provisions of the earlier law, and if any amount becomes recoverable as a result of such appeal, revision, review or reference, the same shall be recovered as an arrear of tax under this Act and amount so recovered shall not be admissible as input tax credit under this Act. (2)Every proceeding of appeal, revision, review or reference relating to any output tax liability initiated whether before, on or after the appointed day, shall be disposed of in accordance with the provisions of the earlier law, and any amount found to be admissible to the claimant shall be refunded to him in accordance with the provisions of the earlier law and shall not be admissible as input tax credit under this Act. (SGST Law)

|

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

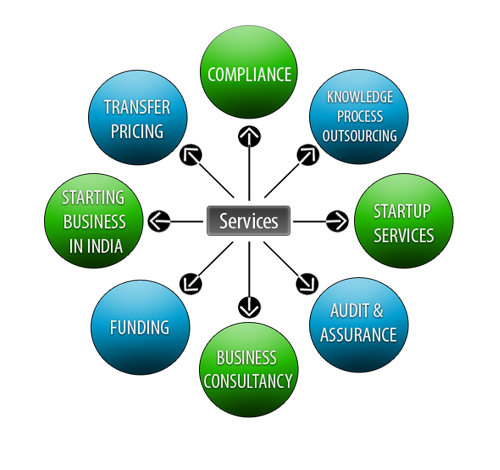

Lets Enhance your Profits by Our Services