|

42. Special provision for deductions in the case of business for prospecting, etc., for mineral oil.—(1) For the purpose of computing the profits or gains of any business consisting of the prospecting for or extraction or production of mineral oils in relation to which the Central Government has entered into an agreement with any person for the association or participation of the Central Government or any person authorised by it in such business (which agreement has been laid on the Table of each House of Parliament), there shall be made in lieu of, or in addition to, the allowances admissible under this Act, such allowances as are specified in the agreement in relation— (a) to expenditure by way of infructuous or abortive exploration expenses in respect of any area surrendered prior to the beginning of commercial production by the assessee ; (b) after the beginning of commercial production, to expenditure incurred by the assessee, whether before or after such commercial production, in respect of drilling or exploration activities or services or in respect of physical assets used in that connection, except assets on which allowance for depreciation is admissible under section 32 : Provided that in relation to any agreement entered into after the 31st day of March, 1981, this clause shall have effect subject to the modification that the words and figures "except assets on which allowance for depreciation is admissible under section 32" had been omitted; and (c) to the depletion of mineral oil in the mining area in respect of the assessment year relevant to the previous year in which commercial production is begun and for such succeeding year or years as may be specified in the agreement; and such allowances shall be computed and made in the manner specified in the agreement, the other provisions of this Act being deemed for this purpose to have been modified to the extent necessary to give effect to the terms of the agreement. (2) Where the business of the assessee consisting of the prospecting for or extraction or production of petroleum and natural gas is transferred wholly or partly or any interest in such business is transferred in accordance with the agreement referred to in sub-section (1), subject to the provisions of the said agreement and where the proceeds of the transfer (so far as they consist of capital sums)— (a) are less than the expenditure incurred remaining unallowed, a deduction equal to such expenditure remaining unallowed, as reduced by the proceeds of transfer, shall be allowed in respect of the previous year in which such business or interest, as the case may be, is transferred; (b) exceed the amount of the expenditure incurred remaining unallowed, so much of the excess as does not exceed the difference between the expenditure incurred in connection with the business or to obtain interest therein and the amount of such expenditure remaining unallowed, shall be chargeable to income-tax as profits and gains of the business in the previous year in which the business or interest therein, whether wholly or partly, had been transferred : Provided that in a case where the provisions of this clause do not apply, the deduction to be allowed for expenditure incurred remaining unallowed shall be arrived at by subtracting the proceeds of transfer (so far as they consist of capital sums) from the expenditure remaining unallowed. Explanation.—Where the business or interest in such business is transferred in a previous year in which such business carried on by the assessee is no longer in existence, the provisions of this clause shall apply as if the business is in existence in that previous year; (c) are not less than the amount of the expenditure incurred remaining unallowed, no deduction for such expenditure shall be allowed in respect of the previous year in which the business or interest in such business is transferred or in respect of any subsequent year or years: Provided that where in a scheme of amalgamation or demerger, the amalgamating or the demerged company sells or otherwise transfers the business to the amalgamated or the resulting company (being an Indian company), the provisions of this sub-section— (i) shall not apply in the case of the amalgamating or the demerged company; and (ii) shall, as far as may be, apply to the amalgamated or the resulting company as they would have applied to the amalgamating or the demerged company if the latter had not transferred the business or interest in the business. Explanation.—For the purposes of this section, "mineral oil" includes petroleum and natural gas. |

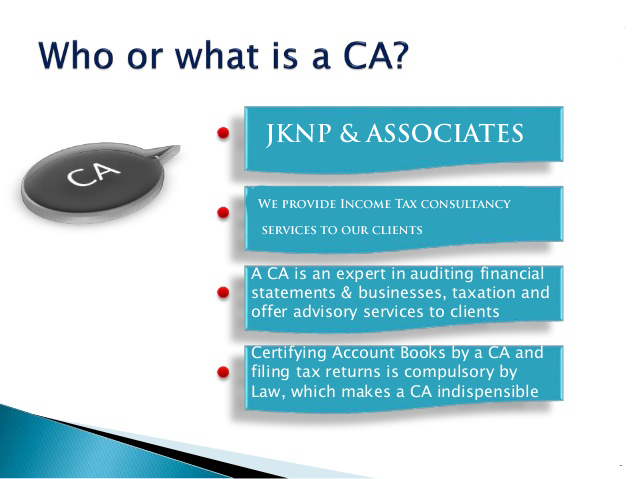

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

We offer comprehensive manual or computerized bookkeeping system

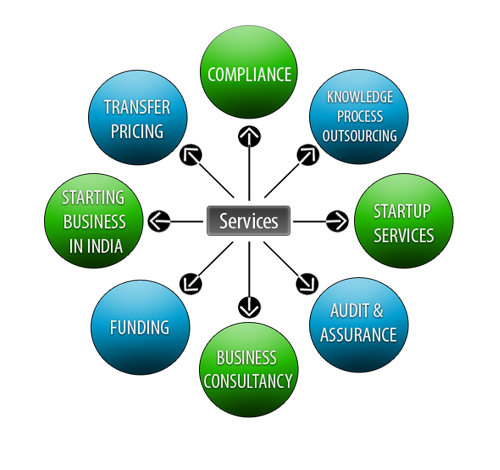

Lets Enhance your Profits by Our Services